Help Get Insurance to Pay for Water Damage

Water damage can be one of the most costly types of damage to repair and replace. Rain, floods, and leaks are unavoidable. When an insurance company receives a water damage claim, they will decide whether or not to pay for the claims based on several factors. If the worst happens, you will have to file for an insurance claim to restore the damage caused by water. Doing regular home maintenance and ensuring that your water system runs smoothly will increase your chances of a payout. The steps of getting the entire insurance claim for water damage in New York City’s apartments include: Step 1 Determine the cause of your water damage and check your homeowner’s insurance policy to see if the insurance company covers the water damage. Insurance Covered Damages You can expect your home insurance to cover sudden or accidental water damage, but not damage caused by neglect or lack of home maintenance. Water damages covered by home insurance include those caused by natural disasters like earthquakes, storms, and hurricanes. You can also claim your homeowner’s policy if there are sudden damages like cracked pipes, a burst in the main water supply, or broken water appliances. Remember, your insurance company might only cover the damage caused by the breaks and not the actual appliances or pipes. Uncovered Damages Individual policies vary on the types of water damages not covered in them. However, the general damages in this category include gradual damage, floods, mold, and damage caused by neglect. In most cases, homeowners need to purchase separate flood insurance because of the extensive damage caused by floods. You can prevent gradual damage and damages caused by neglect. Both damages occur over a long time, giving you time to stop their effect. For example, you can inspect your plumbing system regularly and ensure that it is well-maintained. Sometimes, your water damage might not be a gradual or neglect problem but a mold problem. There are several mold warning signs that you can look out for, including: • You can watch out for mold odor. Most molds produce a persistent musty smell that is not easy to miss • There can also be visible signs of mold growth in your home. Molds come in all colors, so any change you see on your walls or damp places is a warning sign. Ensure you fix all your water leaks to avoid breeding grounds for molds • If you observe water stains or discoloration on your walls, floor, or ceilings, the chances are there is a mold in your home. You should also look out for bubbling, cracking, or peeling paint and wallpapers • Molds may also grow in the aftermath of a flood • Report the claim if the policy covers the damage Step 2 Hire a restoration service to clean up the water and moisture professionally. Determine if you need to leave your home. If the damage is severe, leave your home and allow the restoration to continue. Water damages present the risk of electrocution and unhealthy living conditions inside your home. Step 3 Take photos of the damage and things that you need to replace. Your home restoration team might take these pictures, but it is necessary to have your images. Step 4 Meet with your insurance adjuster, who will evaluate the water damage. The adjuster’s work is to determine the cause of the damage and repair cost. Step 5 Find a contractor to repair the damage once your insurance company processes your claim. In some cases, the company may have its preferred contractors. What can New York Total Damage Restoration (NYTDR) do for you? NYTDR is a restoration company that works directly with your insurance company to repair water damage on your property. It does not matter if the damage is in your kitchen, bathroom, or the whole house. The company will help you get the insurance claim and plan and design your restoration. Licensed repair restoration experts, designers, and construction specialists will remediate and restore your property from start to finish. All you need to do is initiate a free consultation!

Why you need an Experienced Restoration Contractor to Restore and Remodel Your Home

In 2019, there are more homes under insurance covers, compared to three decades ago. It is however interesting to note that in case of property damage, very few homeowners understand the right procedure to claim compensation. The following is a comprehensive guide on approaching home owner insurance claim, working with contractors and other factors you should know in the restoration process. What should you look for in a restoration contractor? Although most homeowners hire contractors based on their availability and locality, it is advisable to have a specific checklist on what you expect. Some of the factors you should look in a restoration contractor include the following. Any contractor should have a practicing license Working with a licensed professional is ideal because of the following factors. First, insurance companies can only work with contractors that have the right documentation to work in the world of renovations. Pundits point out that if the contractor is unlicensed; it is hard for the insurance company to pay for the renovations. Therefore, as a homeowner, asking for practicing license should be the first thing in the hiring process. Check the contractor’s credentials Even though all professionals in the renovation world have the potential to restore your home after property damage, different contractors have a different experience. The more experienced the restoration contractors, the better. In order to verify whether the contractor has the right credentials or not, you should do background checks on different platforms. Job boards, for example, offer some of the best insights on individual contractors. On the other hand, you should review their websites and verify whether the reviews are organic or not. The ideal relationship between homeowners and restoration contractors The nature of your relationship with the contractor determines the restoration speed. In some cases, how you related to the contractor can affect the cost of the whole restoration process. Therefore, redefining the relationship with the contractor is critical for a successful process. Some of the factors you should consider when relating to a contractor include the following. All the suggestions by the contractor should get approval from the insurer. Creating a proper communication channel between the two parties is ideal because of the following two reasons. First, informing the insurance company on the restoration process gives them ample time to calculate the claim and prepare for payments. In case the cost of restoration goes beyond the insured amount, the insurance company communicates — through writing — the amount they are obligated to pay as a homeowner. Second, it is a regulation in the world of insurance to inform the insurer on the restoration process. According to insurance pundits, creating a good communication channel between the two parties eliminates administrative errors in the compensation process — and future surprises of unpaid claims. Also, most insurance covers have clauses that require the homeowner to inform the insurer on the renovation process. Insist on written agreement with contractors Written agreements are not only part of the insurance requirements, but they also protect your interests as a homeowner. Therefore, any agreement between you and the contractor should be in writing. Putting all the agreements on writing also creates a good rapport between you — as a homeowner — and other parties in the restoration process. Is there a difference between restoration and general contractors? Not all contractors have the same abilities in restoring your home to its initial status. Although general contractors are relatively inexpensive, they might fail to meet the following threshold. Restoration projects are technical, and therefore, a contractor must have the right set of equipment. Working with a general contractor is, therefore, not advisable. Second, working with a specialized contractor is also ideal because of experience. Experience differentiates a restoration contractor from a mainstream contractor. The homeowner gets the value for money in the following way. In less than an hour, a restoration contractor can estimate the repair time, and in some cases, they can estimate the value of restoration. Thirdly, with the Institute of Inspection Cleaning and Restoration Certification, the homeowner is certain that the process is within the stipulated guidelines. The certification also gives the contractor the power to negotiate the deals on your behalf with the insurance company. What is the right procedure for filling a home owner’s insurance claim? In case of property damage from water, mold, fire or asbestos, you should follow these three steps. Make a formal notification to the insurance company: Making an official notification to the insurance company is the first and the most important step in the claim process. Different companies have different time requirements for making the notification. However, the universal rule dictates that you should make the notification as soon as possible. There are consequences of failing to make formal communication to the insurance company. In some cases, the insurance company may fail to honor the claim because of late communication. In 2019, making a formal notification is easy. Depending on where you are as a homeowner, you can report through a call or using an online platform. During the notification process, being specific in terms of details is critical. The wrong information is not only a ground for claim dismissal, but the insurance company can sue you as a homeowner. Secure your home from further damages: After making a formal communication to the insurance company, the next important step in securing your property from further damages such as water mitigation. The homeowner has a set of responsibilities such as saving lives within the property and more importantly, ensuring that there are no more damages. In some cases, you have an obligation as a homeowner to contact the government agencies in charge of your community. Firefighters, for example, can assist you in preventing more fire or smoke damages and therefore shortening the claim process. In case there were people within the property, calling for an ambulance is vital. During this process, ensure you keep the communication records with authorized professionals — for future proof that the damages on the

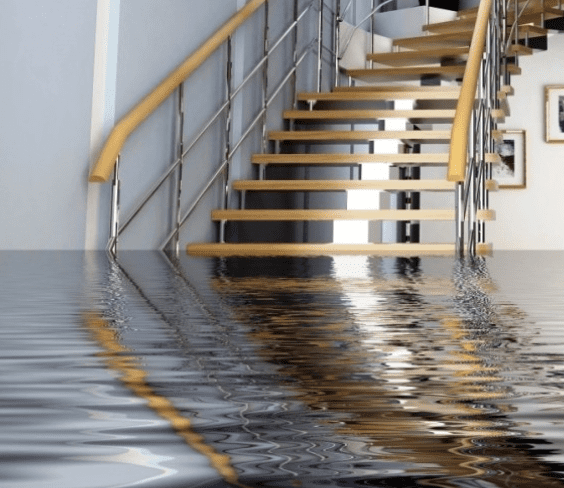

Flooded basement – will my insurance cover?

Flooded basements – what to do if a basement floods? Few things in a homeowner’s life are so stressful as a flooded basement. Unfortunately for your insurance, this is also among the most unclear situations you can face regarding insurance coverage and claims. Some causes of flooding the home owner’s insurance policy will cover, while others it will not. In those cases, you would need to have actual flood insurance to be covered. Emergency First Actions Following Basement Flooding There are a series of practical steps you should take if you find your basement unexpectedly flooded. The first thing to do every time is to turn off all power surrounding the area. This includes both gas and electricity. A golden rule is to not ever submerge yourself in any flooded area when the power is still turned on. If you can not turn off the electricity with certainty, then you should call an electrician first. When the water is not caused by rain, you should take immediate steps to rectify the situation. If a storm is causing the flooding, it is always best to wait until the storm is over before you start the work. No matter the cause of the water, you always need to wear gloves and boots as protective gear. Be careful moving and walking around flooded places as they often can cause slipping hazards. These are some steps you should follow in general when you are dealing with a flooded area: 1. Ascertain where the water is coming from – In cases where a burst pipe is to blame, turn off all water sources to the basement. 2. Many basements come equipped with a floor drain – ensure that it has not been clogged in the flood. Maintaining an open and fully working floor drain will help to remove the water quickly. 3. Begin manually removing the basement water – there are several types of pumps that are handy for forcing the water out of a basement. Pool pumps, sump pumps, and even wet/dry vacuums are all potential solutions for the job. You find sump pumps down in the lowest section of the basement. These function by draining the water out of the house. Sump pumps generally prevent water from entering through the ground level and coming into a home. An unexpected sump pump failure could lead to floods in more than just the basement. Once the majority of the water is out, you can utilize sponges and cloths to soak up the rest of the water. 4. Remove all damaged things from the basement over to a ventilated area for drying – Sunny spots are naturally best if you have them. Never attempt to dry wet items in the basement which is already a damp space. In well-ventilated areas, items generally require about 48 hours to dry completely. If they stay wet longer than this, they will begin to suffer from mildew and mold accumulation. You should carefully inspect them thoroughly after the 48 drying period to determine if they need to be thrown out. Wet cardboard boxes are especially good candidates for bacteria and mold. You might salvage what was in the boxes before throwing the boxes themselves away. Calling In A Professional Is Always A Sensible and Safe Idea Because of all the things that can go wrong in such a cleanup job, it is never a bad idea to bring in a professional. You should never touch anything electrical that is wet, even after electricity has been both turned off and disconnected. Stereos, televisions, and lamps are all extremely dangerous things to touch in floods. Electrical equipment should be left to dry where it is standing or resting. Electricians are the best professionals to call in cases where thee are potentially damaged electronics and electrical appliances. Does Insurance Cover Flooded Basements? Once you have addressed the damage, the nagging, critical question arises: Who is going to pay for all the mess, cleanup, and damage? The question about insurance responsibility depends entirely on what caused the flooding in the first place. Here are some causes that would be covered by typical homeowner’s insurance policies: Broken Appliance Flooding – when the A/C, washing machine, or refrigerator malfunctioned and caused a room to flood, standard homeowner’s insurance policies will cover the water damage. The caveat surrounds proper maintenance. If the appliances are not properly maintained, then they may argue is your fault. Leaking Water Heater Flooding – Leaky water heaters would be covered by a homeowner’s insurance policy. Once again, the insurance company may try to disqualify the claim based on any poorly maintained water heaters. Bursting Freezing Pipe Leaks – Insurance policies cover bursting pipes that freeze. This includes appliances, sprinklers, and A/C/ units. The only requirement is that you must be occupying the house when it floods. Overflowing Pools, Tubs, Sinks Floods – If something overflowed, your insurance policy will also cover this damage. They call this “sudden and accidental” so all destroyed items will be replaced. Other incidents will not be covered by standard Homeowner’s Insurance Policies. These include situations like: Floods from heavy rains and storm surge – nature caused flooding is never covered under a standard Home Owner’s Insurance Policy. Only flood insurance will help in these natural causes. A good sump pump is the best remedy for these cases. Sewage Backing Up Floods – When your external sewer backs up into the basement, you can not count on your Homeowner’s Insurance Policy. Such a sewage backup will be among the most expensive disasters your home can suffer from. Sewage backups can cost even hundreds of thousands of dollars in repairs. Underground Water Seepage – This is usually not covered. Saturated ground can force water into the basement. The importance of using a professional in terms of ensuring water removal is done right can not be overstated. Steps To Ensure No Mold Occurs and Complete Restoration Results There are a number of steps you should follow to make sure

What do Insurance Adjustors Do?

Experiencing damage to your home is disconcerting and, depending on the extent of the devastation, can be downright frightening and traumatic. Whether the destruction comes in the form of fire, water damage, smoke, or mold, the effect is troublesome in the extreme, as your house is your most important investment. After the initial shock of the catastrophe has worn off, you realize that you had better call your home insurance agent because now is the time that all those monthly premiums pay off. At this point, you may also begin to feel a little uneasy. You may wonder if your coverage is sufficient to take care of the damage and you might even wonder if you are going to get a fair shake from your insurance company. There will be a claims adjuster coming to your home to assess the property loss, and you could wonder if this person will make sure that your compensation is adequate. Below, we are going to look at the claims adjusters’ responsibilities, and what actions that you can take to make sure that you maximize the benefits of your policy. What is the Function of a Home Insurance Claims Adjuster? Insurance claims adjusters have several job responsibilities, and most of them have to do with determining how much money is paid out on the claim the policyholder has filed. They will examine the damage to your home, consult with trade professionals, and submit a recommendation to the corporate office specifying a figure for settlement of the claim. However, that is not all that they will be doing. Remember, the claims adjuster does not work for you, the insurance company that holds your policy is their employer. Technically, the claims adjuster is investigating for the insurance company, and this investigation has different components. You might be surprised to learn that part of what the adjuster is doing is gathering evidence to support the settlement if a court battle ensues. The adjuster may also function as a negotiator if you do not accept the settlement, to try and find common ground and avoid a court case. The adjuster will also interview any witnesses, police and fire personnel, and hospital staff if there was an injury. He or she examines the title of the property to ensure that the claimant has clear title to the home. Critically, the adjuster determines liability – in other words, are you in any way liable for the damage to the house. Another function of the claims adjuster is to evaluate your coverage to ascertain limitations to restoration from a financial perspective. In other words, if your policy covers $25,000 of damage, but the cost to repair the damage is $30,000, there is a $5,000 shortfall. Also, your policy may pay for temporary housing or it may not. The job of the claims adjuster is to determine what your policy covers and what you will have to pay out of pocket. The insurance company that holds your policy is a giant corporation, and they want to settle your claim fairly, but for the least amount of money possible. The adjuster may seem like your best friend and savior at first, but there is a possibility that things may become adversarial and your job is to involve yourself in every step of the claims process, documenting everything, and advocating your position. How Does a Claims Adjuster Arrive at a Settlement Amount? Most states require that insurance claims adjusters be licensed, so they have to complete a course, get a certificate, submit it to the state department of insurance, and then must pass an exam for licensing. Also, claims adjusters receive additional training from their companies that is ongoing. This licensing means that the adjuster is qualified to inspect property damage and estimate replacement costs. He or she will come into your home and complete a thorough examination of all the loss and take a lot of pictures. After the adjuster finishes the analysis, they will go back to their office to work on the claim. Increasingly, many insurance companies use a type of software to process claims called Xactimate. This software, used by claims adjusters, calculates damage, rebuilding, and repair costs. Xactimate also produces loss estimates and settlement proposals. Because the software operates on a cookie-cutter premise, it often comes up with low settlement offers for homes, such as historical or custom-built homes. Contractors do not use Xactimate, so there can be disparities between their estimates and the adjuster’s estimate. Make sure to stick with your contractor, and if the adjuster will not budge, then it’s a different ball game that we will discuss later in the article. What is the Right Way to Deal with a Home Insurance Claims Adjuster? Documentation throughout the claims process is crucial, and one of the best ways to keep everything on the record is to communicate by email. Emails are irrefutable evidence you can use for backup in a disagreement. Avoid phone conversations, because you cannot document them. The insurance company, however, will record conversations so that they can use them against you if necessary. Do not ever allow yourself to go on the record in any way, and do not sign anything until you are satisfied with the settlement. Choose the Contractor Yourself. Home insurance claims adjusters are more than happy to provide you with contractors that they regularly work with to repair the damage to your home. The foolishness of agreeing to these terms should be apparent, but some folks fall for it, so make sure that you are not one of them. Find a reputable contractor if you do not already have one in mind, preferably one that has some experience dealing with aggressive claims adjusters. Feel free to get several estimates if you would like. Contractors that work with insurance companies are sometimes entities that have a hard time finding business any other way. These contractors are beholden to the insurance company and understand that part of their job is to

What will it cost? Top 6 Questions to ask before a home damage restoration

Accidents can and do happen. You’ve just purchased the apartment of your dreams in New York’s historic yet on-trend Carnegie Hill neighborhood. After five paychecks’ worth of savings, your furniture and fixtures are ready to be put on display. Let the dinner parties begin, right? Now, imagine that one of your apartment’s old pipes burst while you were visiting your best friend in Boston for the weekend. Rather than getting ready to host your first dinner party, you’re now absorbed with cleaning up water damage in your apartment. This tale of woe can have a happier ending with the right insurance. Let’s explore the insurance products that cover home damage from water, mold, smoke, and asbestos. Water and Mold Damage Recovery Insurance In the above scenario, the plumbing problem was caused by gradual damage to the pipes that was a result of long-term corrosion. Depending on your insurance company and the policy that you carry, your standard homeowner’s insurance policy may not cover this accident. Many insurance policies cover sudden damage to pipes but not gradual damage to them. Here are five key questions that you need to ask your insurance company about water damage. What is gradual damage? Is there an insurance addendum that I can get to cover gradual damage? What is the procedure for filing a water damage claim? Does my policy cover damage from mold? Does my policy cover the entire bill for mold remediation? Gradual damage, which is usually not covered under most standard insurance policies, is harm that happens slowly over a long period. Old, rusted pipes that burst will likely get categorized as gradual damage because the corrosion happened over many years. The homeowner had time to get the plumbing inspected and fixed before a costly accident happened. Mold that develops and spreads through your home over a long period due to a hidden pipe leak usually isn’t covered by your standard insurance policy. Many policies will, however, cover mold damage and pay for professional mold remediation if the mold is a result of sudden water damage. Mold remediation is expensive, and it’s common for standard policies to only pay a portion of the cost. Smoke Damage Insurance Policies While not all home insurance products are the same, most of them cover repair or replacement costs for household items that are damaged by smoke, soot, or ash. The problem gets a little complex if you have smoke damage that is caused by a fire at your neighbor’s house. Here are some actions to take if you have smoke damage. Review your insurance policy Take pictures of damaged items Hire a professional smoke damage restoration professional to clean Some insurance policies don’t cover smoke damage, and a review of your policy will unveil this gap in coverage. If your policy covers smoke damage, you’ll need proof of the damage to make your claim. It’s best not to rely on evaluations from claims adjusters. You need to document every item that has been damaged and do an assessment of each piece’s value. Cleaning up smoke and soot can be hazardous to your health if you don’t have the proper equipment or training. It’s best to hire a professional to restore your home and furnishings. Asbestos Insurance Coverage If your home was built before 1980, there’s a chance that it contains asbestos in its insulation, siding, and other building materials. This substance is a known carcinogen, and its tiny, sharp fibers cause severe lung damage when inhaled. Undisturbed asbestos in your home doesn’t pose a significant health risk. If you’re doing a remodeling project that will disturb the old asbestos, it’s best to have the asbestos removed by a professional. Here are some questions that you should ask your insurance company about coverage for asbestos removal. Does my standard policy cover asbestos removal? Does my standard policy cover asbestos removal? Is there extra insurance that I can get to cover asbestos liability? What’s covered under asbestos liability coverage? Most insurance companies will not cover asbestos removal from a home just because you want to do a safe home remodel. If your home is damaged by a covered item such as a storm and its asbestos is disturbed, then the insurance company would pay for asbestos removal services as part of the storm damage. While asbestos liability insurance is a popular solution in other countries, most U.S. insurance companies don’t offer this coverage. If a company writes an asbestos liability policy, it will likely cover asbestos-related medical expenses for these three groups: Property owners who live in a home that has asbestos Contractors who work on the home that has asbestos Asbestos abatement professionals who are hired to remove asbestos from the home Not sure whether and how much you will be covered? Call NYTDR today and let us help you navigate through your damage restoration.